2. Functional Forms Of Regression Models#

suppressPackageStartupMessages({

library(tidyverse)

library(tidymodels)

library(readxl)

library(multcomp)

library(car)

})

Cobb Douglas Function#

Log-log model (Double log) (Constant elasticity) (log-linear)#

\begin{align} \text{output} &= \beta_0 \text{labor}^{\beta_1}\text{capital}^{\beta_2}\ \ln \text{output}_i &= \ln \beta_0 + \beta_1 \ln \text{labor}_i + \beta_2 \ln \text{capital}_i +u \end{align}

labor input (worker hours, in thousands),

and capital input (capital expenditure, in thousands of dollars) for the US manufacturing sector.

The data is cross-sectional, covering 50 states and Washington, DC, for the year 2005.

df <- read_excel("data/Table2_1.xls")

head(df)

| obs | output | labor | capital | lnoutput | lnlabor | lncapital | lnoutlab | lncaplab | outputstar | capitalstar | laborstar |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> |

| 1 | 38372840 | 424471 | 2689076 | 17.46286 | 12.958599 | 14.80471 | 4.504261 | 1.846109 | -0.1079874 | 0.06368887 | 0.1343891 |

| 2 | 1805427 | 19895 | 57997 | 14.40631 | 9.898224 | 10.96815 | 4.508084 | 1.069923 | -0.9230660 | -0.90551400 | -0.9410533 |

| 3 | 23736129 | 206893 | 2308272 | 16.98251 | 12.239957 | 14.65201 | 4.742552 | 2.412053 | -0.4342360 | -0.07658678 | -0.4439759 |

| 4 | 26981983 | 304055 | 1376235 | 17.11068 | 12.624964 | 14.13486 | 4.485716 | 1.509898 | -0.3618868 | -0.41991854 | -0.1857003 |

| 5 | 217546032 | 1809756 | 13554116 | 19.19792 | 14.408703 | 16.42220 | 4.789218 | 2.013498 | 3.8857391 | 4.06601191 | 3.8167481 |

| 6 | 19462751 | 180366 | 1790751 | 16.78401 | 12.102743 | 14.39815 | 4.681270 | 2.295402 | -0.5294886 | -0.26722449 | -0.5144899 |

model <- lm(lnoutput~ lnlabor+ lncapital, data = df)

tidy(model)

glance(model)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 3.8875990 | 0.39622813 | 9.811517 | 4.704731e-13 |

| lnlabor | 0.4683318 | 0.09892588 | 4.734169 | 1.980888e-05 |

| lncapital | 0.5212795 | 0.09688703 | 5.380281 | 2.183108e-06 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9641754 | 0.9626828 | 0.266752 | 645.9316 | 1.996821e-35 | 2 | -3.426703 | 14.85341 | 22.58071 | 3.415518 | 48 | 51 |

interpretation of the coefficient of lnlabor of about 0.47 is that if we increase the labor input by 1%, on average, output goes up by about 0.47 %, holding the capital input constant

interpretation of the coefficient of lncapital of about 0.52 is that if we increase capital input by 1%, on average, the output increases by about 0.52%, holding the labot input constant

tidy_model <- tidy(model)

colnames(tidy_model)

rownames(tidy_model)

- 'term'

- 'estimate'

- 'std.error'

- 'statistic'

- 'p.value'

- '1'

- '2'

- '3'

(intercept <- tidy_model[[1,'estimate']])

exp(intercept)

(beta_1 <- tidy_model[[2, 'estimate']])

(beta_2 <- tidy_model[[3, 'estimate']])

(return_to_scale <- beta_1 + beta_2)

linear model#

model2 <- lm(output~ labor + capital, data = df)

tidy(model2)

glance(model2)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 2.336216e+05 | 1.250364e+06 | 0.1868428 | 8.525714e-01 |

| labor | 4.798736e+01 | 7.058245e+00 | 6.7987660 | 1.496564e-08 |

| capital | 9.951891e+00 | 9.781165e-01 | 10.1745459 | 1.433023e-13 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9810653 | 0.9802763 | 6300694 | 1243.514 | 4.510314e-42 | 2 | -869.2846 | 1746.569 | 1754.297 | 1.90554e+15 | 48 | 51 |

tidy_model2 <- tidy(model2)

as.numeric(tidy_model2$estimate)

as.numeric(tidy_model2$p.value)

- 233621.609858679

- 47.987358368403

- 9.95189072306451

- 0.852571362047071

- 1.49656436518791e-08

- 1.43302279569064e-13

If labor input increases by a unit, the average output goes up by about 48 units, holding capital constant

Linear restriction#

Manual calculation#

\(RSS_R\)= residual sum of squares from the restricted regression

\(RSS_{UR}\)= residual sum of squares from the unrestricted regression

\(m\) = number of linear restrictions (1 here)

\(k\) = number of parameters in the unrestricted regression (3 here)

model3 <- lm(log(output/labor) ~ log(capital/labor), data = df)

tidy(model3)

glance(model3)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 3.7562419 | 0.18536786 | 20.263717 | 1.816211e-25 |

| log(capital/labor) | 0.5237564 | 0.09581225 | 5.466487 | 1.535206e-06 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.3788227 | 0.3661456 | 0.2644047 | 29.88247 | 1.535206e-06 | 1 | -3.501733 | 13.00347 | 18.79894 | 3.425582 | 49 | 51 |

summary(model3)

Call:

lm(formula = log(output/labor) ~ log(capital/labor), data = df)

Residuals:

Min 1Q Median 3Q Max

-0.43644 -0.12465 -0.05083 0.04356 1.23075

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.75624 0.18537 20.264 < 2e-16 ***

log(capital/labor) 0.52376 0.09581 5.466 1.54e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.2644 on 49 degrees of freedom

Multiple R-squared: 0.3788, Adjusted R-squared: 0.3661

F-statistic: 29.88 on 1 and 49 DF, p-value: 1.535e-06

anova(model)

| Df | Sum Sq | Mean Sq | F value | Pr(>F) | |

|---|---|---|---|---|---|

| <int> | <dbl> | <dbl> | <dbl> | <dbl> | |

| lnlabor | 1 | 89.864812 | 89.86481250 | 1262.91571 | 3.933902e-36 |

| lncapital | 1 | 2.059801 | 2.05980082 | 28.94742 | 2.183108e-06 |

| Residuals | 48 | 3.415518 | 0.07115662 | NA | NA |

colnames(anova(model))

rownames(anova(model))

- 'Df'

- 'Sum Sq'

- 'Mean Sq'

- 'F value'

- 'Pr(>F)'

- 'lnlabor'

- 'lncapital'

- 'Residuals'

(RSSur <- anova(model)["Residuals","Sum Sq"])

(DFur <-anova(model)["Residuals","Df"])

anova(model3)

(RSSr <- anova(model3)["Residuals","Sum Sq"])

| Df | Sum Sq | Mean Sq | F value | Pr(>F) | |

|---|---|---|---|---|---|

| <int> | <dbl> | <dbl> | <dbl> | <dbl> | |

| log(capital/labor) | 1 | 2.089079 | 2.08907903 | 29.88247 | 1.535206e-06 |

| Residuals | 49 | 3.425582 | 0.06990984 | NA | NA |

(f = ((RSSr-RSSur)/1)/(RSSur/(DFur)))

(p_value <- pf(f, 1, DFur, lower.tail = FALSE))

conclusion: The restirction was correct, can use restricted model

using car package#

unrestricted_model <- lm(log(output) ~ log(labor) + log(capital), data = df)

hypothesis <- "log(labor) + log(capital) = 1"

(test_result <- linearHypothesis(unrestricted_model, hypothesis))

| Res.Df | RSS | Df | Sum of Sq | F | Pr(>F) | |

|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | |

| 1 | 49 | 3.425582 | NA | NA | NA | NA |

| 2 | 48 | 3.415520 | 1 | 0.01006201 | 0.1414065 | 0.7085437 |

Log-lin model (growth model)#

df2 <- read_excel("data/Table2_5.xls")

head(df2,3)

tail(df2,3)

| rgdp | time | time2 | lnrgdp |

|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> |

| 2501.8 | 1 | 1 | 7.824766 |

| 2560.0 | 2 | 4 | 7.847763 |

| 2715.2 | 3 | 9 | 7.906621 |

| rgdp | time | time2 | lnrgdp |

|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> |

| 10989.5 | 46 | 2116 | 9.304695 |

| 11294.8 | 47 | 2209 | 9.332098 |

| 11523.9 | 48 | 2304 | 9.352179 |

Data shows Real GDP for USA for 1960-2007

model4 <- lm(lnrgdp ~ time, data = df2)

tidy(model4)

glance(model4)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 7.87566236 | 0.0097591072 | 807.00644 | 3.931863e-97 |

| time | 0.03148955 | 0.0003467383 | 90.81649 | 1.519344e-53 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9944536 | 0.994333 | 0.03327965 | 8247.634 | 1.519344e-53 | 1 | 96.24722 | -186.4944 | -180.8808 | 0.05094662 | 46 | 48 |

Time Coefficient: Real GDP increases at raate 3.15% per year

Intercept result: exp(7.87) = 2632.27 is the beginning value of real GDP at the beginning of 1960

compound interest: \(\beta_2 = \ln(1+r)\). r = exp(\(\beta_2\))-1, r = 3.2%

Compare it with linear model#

model5 <- lm(rgdp ~ time, data = df2)

tidy(model5)

glance(model5)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 1664.2176 | 131.998983 | 12.60781 | 1.570394e-16 |

| time | 186.9939 | 4.689886 | 39.87174 | 2.523710e-37 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9718784 | 0.9712671 | 450.1314 | 1589.756 | 2.52371e-37 | 1 | -360.3455 | 726.691 | 732.3046 | 9320439 | 46 | 48 |

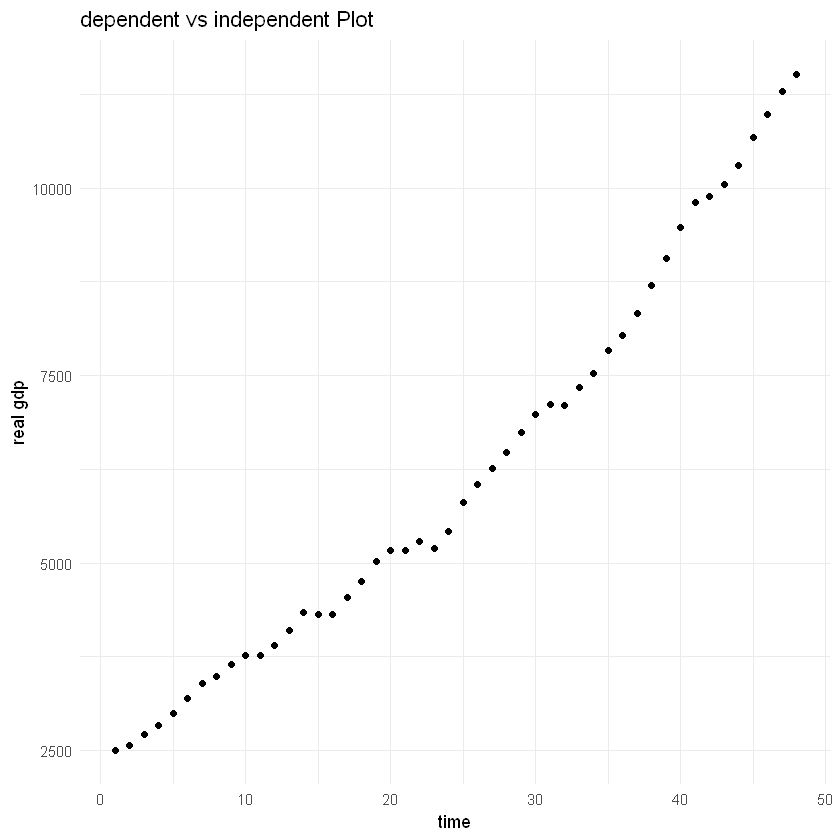

Time coefficient: real gdp increases by $187 billion per year showing positive trend

df2$residuals <- residuals(model5)

df2$fitted_values <- fitted(model5)

ggplot(df2, aes(x = time, y = rgdp)) +

geom_point() +

labs(title = "dependent vs independent Plot",

x = "time",

y = "real gdp") +

theme_minimal()

Lin-LOg model#

df3 <- read_excel("data/Table2_8.xls")

head(df3,3)

tail(df3,3)

| fdho | expend | sfdho | lnexpend | expend_rec | expend2 |

|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> |

| 6475 | 40516.75 | 0.15981045 | 10.609470 | 2.468115e-05 | 1641607040 |

| 3146 | 33540.50 | 0.09379705 | 10.420509 | 2.981470e-05 | 1124965120 |

| 1632 | 5181.85 | 0.31494543 | 8.552917 | 1.929813e-04 | 26851570 |

| fdho | expend | sfdho | lnexpend | expend_rec | expend2 |

|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> |

| 5811 | 31922.20 | 0.1820363 | 10.371057 | 3.132616e-05 | 1019026816 |

| 4594 | 25357.25 | 0.1811711 | 10.140820 | 3.943645e-05 | 642990144 |

| 2108 | 7313.60 | 0.2882302 | 8.897491 | 1.367316e-04 | 53488748 |

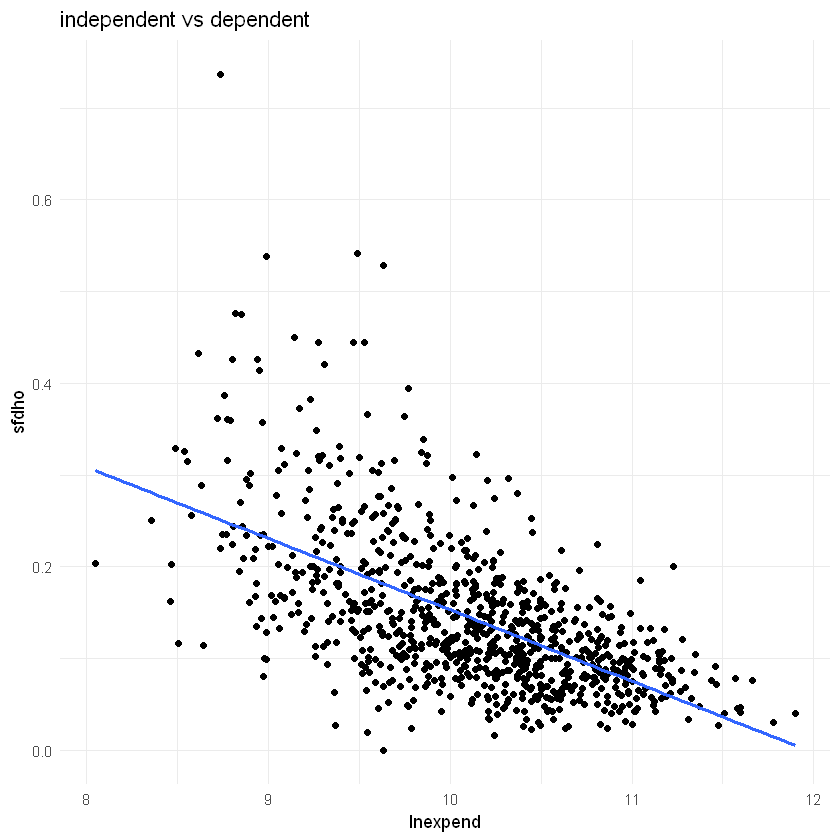

Engel expenditure function theory: the total

expenditure that is devoted to food tends to increase in arithmetic progression as

total expenditure increases in geometric proportion.

In other words: share of expenditure on food decreases as total expenditure increases

Expend: total household expenditure

SFDHO: share of food expenditure

869 US households in 1995

model6 <- lm(sfdho ~ lnexpend, data = df3)

tidy(model6)

glance(model6)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 0.93038679 | 0.036366542 | 25.58359 | 5.360528e-108 |

| lnexpend | -0.07773725 | 0.003590929 | -21.64823 | 2.011079e-83 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.3508757 | 0.350127 | 0.06875045 | 468.6456 | 2.011079e-83 | 1 | 1094.493 | -2182.986 | -2168.684 | 4.097984 | 867 | 869 |

lnexpend coefficient: -0.08:

if expenditure increases by 1%, on average, sfhdo decreases by 0.0008 units

if expenditure increases by 100%, on average, sdfho decreases by 0.08 units

df3$residuals <- residuals(model6)

df3$fitted_values <- fitted(model6)

ggplot(df3, aes(x = lnexpend, y = sfdho)) +

geom_point() +

geom_smooth(method = 'lm',formula = y ~ x, se = FALSE) +

labs(title = "independent vs dependent",

x = "lnexpend",

y = "sfdho") +

theme_minimal()

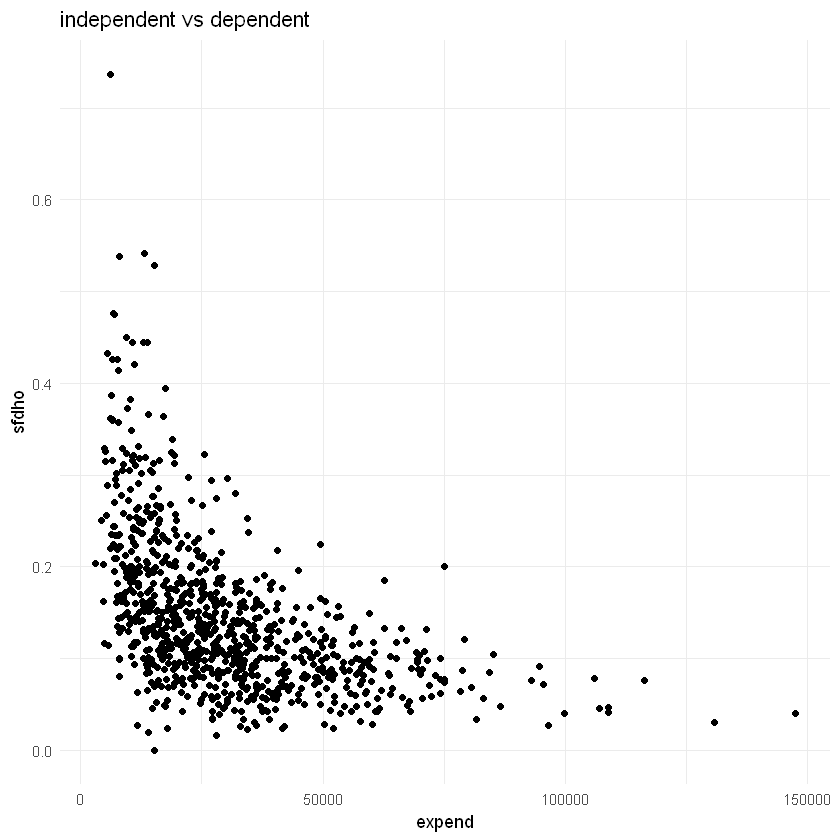

Reciprocol models#

Note: $\( \frac{dY_i}{dX_i} = -\beta_1\left(\frac{1}{X_i}^2\right) \)$

model7 <- lm(sfdho ~ I(1/expend), data = df3)

tidy(model7)

glance(model7)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 7.726305e-02 | 0.004011685 | 19.2595 | 4.376382e-69 |

| I(1/expend) | 1.331338e+03 | 63.957133553 | 20.8161 | 2.303454e-78 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.3332359 | 0.3324669 | 0.06967833 | 433.31 | 2.303454e-78 | 1 | 1082.843 | -2159.686 | -2145.384 | 4.209346 | 867 | 869 |

Intercept coeff: if expend increases indefinitely, sfdho will equal 8% or 0.08

slope coeff: positive slope, rate of change of sfdho with respect to expenditure is negative

ggplot(df3, aes(x = expend, y = sfdho)) +

geom_point() +

labs(title = "independent vs dependent",

x = "expend",

y = "sfdho") +

theme_minimal()

lin-log model performed better than reciprocol model based on \(R^2\), both have same dependent variable so we can compare using it

summary(model6)$r.squared

summary(model7)$r.squared

Polynomial regression model#

model8 <- lm(rgdp ~ time + I(time^2), data = df2)

tidy(model8)

glance(model8)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 2651.380622 | 69.4908403 | 38.15439 | 6.449733e-36 |

| time | 68.534362 | 6.5421140 | 10.47587 | 1.187953e-13 |

| I(time^2) | 2.417542 | 0.1294432 | 18.67647 | 7.969017e-23 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9967866 | 0.9966438 | 153.8419 | 6979.431 | 8.066871e-57 | 2 | -308.2845 | 624.5691 | 632.0539 | 1065030 | 45 | 48 |

The rate of change of RGDP increases with an increasing rate

unlike the linear model that showed constant rate $187

Log-lin model with quadratic trend#

The model increases with a decreasing rate

unlike the quadratic RGDP model (model 8)

model9 <- lm(lnrgdp ~ time + I(time^2), data = df2)

tidy(model9)

glance(model9)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 7.8334797935 | 1.275348e-02 | 614.223018 | 6.228568e-90 |

| time | 0.0365514617 | 1.200658e-03 | 30.442868 | 1.147864e-31 |

| I(time^2) | -0.0001033042 | 2.375639e-05 | -4.348483 | 7.756188e-05 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9960946 | 0.9959211 | 0.02823421 | 5738.809 | 6.492039e-55 | 2 | 104.6665 | -201.333 | -193.8482 | 0.03587268 | 45 | 48 |

rate of growth of RGDP decreases at rate 0.0002 per unit of time

Comparing linear and log-log (log-linear) models#

compare_models <- function(df, dependent_var, independent_vars) {

library(dplyr)

library(broom)

# Step 1: Compute the geometric mean (GM) of the dependent variable

geom_mean <- exp(mean(log(df[[dependent_var]])))

# Step 2: Transform the dependent variable

df <- df %>%

mutate(transformed_output = .[[dependent_var]] / geom_mean,

log_output = log(transformed_output))

# Create formula strings for the models

independent_vars_formula <- paste(independent_vars, collapse = " + ")

linear_formula <- as.formula(paste("transformed_output ~", independent_vars_formula))

log_linear_formula <- as.formula(paste("log_output ~", paste("log(", independent_vars, ")", collapse = " + ")))

# Step 3: Estimate the linear model using transformed_output

linear_model <- lm(linear_formula, data = df)

linear_model_tidy <- tidy(linear_model)

linear_model_rss <- sum(residuals(linear_model)^2)

# Step 4: Estimate the log-linear model using log_output

log_linear_model <- lm(log_linear_formula, data = df)

log_linear_model_tidy <- tidy(log_linear_model)

log_linear_model_rss <- sum(residuals(log_linear_model)^2)

# Ensure residuals sum of squares matches expected values by directly comparing them

rss1 <- sum((df$transformed_output - predict(linear_model))^2)

rss2 <- sum((df$log_output - predict(log_linear_model))^2)

# Number of observations

n <- nrow(df)

# Compute the likelihood ratio test statistic

lambda <- (n / 2) * log(rss1 / rss2)

# Compute the p-value from the chi-square distribution with 1 degree of freedom

p_value <- pchisq(lambda, df = 1,)

# Print results

print(linear_model_tidy)

print(log_linear_model_tidy)

# Compare RSS

print(paste("RSS for linear model:", rss1))

print(paste("RSS for log-linear model:", rss2))

print(paste("Lambda (test statistic):", lambda))

print(paste("P-value:", p_value))

return(list(

linear_model = linear_model,

log_linear_model = log_linear_model,

linear_model_rss = rss1,

log_linear_model_rss = rss2,

lambda = lambda,

p_value = p_value

))

}

compare_models(df, "output", c("labor", "capital"))

# A tibble: 3 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 0.0103 0.0549 0.187 8.53e- 1

2 labor 0.00000211 0.000000310 6.80 1.50e- 8

3 capital 0.000000437 0.0000000429 10.2 1.43e-13

# A tibble: 3 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) -13.1 0.396 -32.9 1.30e-34

2 log(labor) 0.468 0.0989 4.73 1.98e- 5

3 log(capital) 0.521 0.0969 5.38 2.18e- 6

[1] "RSS for linear model: 3.67211242597136"

[1] "RSS for log-linear model: 3.41552013886784"

[1] "Lambda (test statistic): 1.84715109633792"

[1] "P-value: 0.825884897403209"

$linear_model

Call:

lm(formula = linear_formula, data = df)

Coefficients:

(Intercept) labor capital

1.026e-02 2.107e-06 4.369e-07

$log_linear_model

Call:

lm(formula = log_linear_formula, data = df)

Coefficients:

(Intercept) log(labor) log(capital)

-13.0538 0.4683 0.5213

$linear_model_rss

[1] 3.672112

$log_linear_model_rss

[1] 3.41552

$lambda

[1] 1.847151

$p_value

[1] 0.8258849

Regression on standardized variables#

standardize_variables <- function(df, dependent_var, independent_vars) {

df[[dependent_var]] <- scale(df[[dependent_var]], center = TRUE, scale = TRUE)

for (var in independent_vars) {

df[[var]] <- scale(df[[var]], center = TRUE, scale = TRUE)

}

return(df)

}

df_standardized <- standardize_variables(df, "output", c("labor", "capital"))

model10 <- lm(output ~ labor + capital, data = df_standardized)

tidy(model10)

glance(model10)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 2.433157e-17 | 0.01966566 | 1.237262e-15 | 1.000000e+00 |

| labor | 4.023881e-01 | 0.05918546 | 6.798766e+00 | 1.496564e-08 |

| capital | 6.021852e-01 | 0.05918546 | 1.017455e+01 | 1.433023e-13 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9810653 | 0.9802763 | 0.1404409 | 1243.514 | 4.510314e-42 | 2 | 29.29145 | -50.58289 | -42.85559 | 0.9467354 | 48 | 51 |

intercept = tidy(model10)[[1,2]]

ifelse(intercept < .Machine$double.eps,

paste(intercept, "is almost zero"),

paste(intercept, "is not almost zero"))

labor coefficient: if labor increases by one standard deviation unit, average value of output goes up by about 0.40 standard deviation units, cetris paribus

capital coefficient: if labor increases by one standard deviation unit, average value of output goes up by about 0.60 standard deviation units, cetris paribus

Note: same \(R^2, t, F\)

does not mean that capital is more important than labor

Regression through the origin: zero intercept model#

capital asset price model (CAPM)#

\begin{align} (ER_i-r_f) &= \beta_i(ER_m-r_f)\ ER_i &= \text{expected rate of return on security}\ ER_m &= \text{expected rate of return on market portfolio}\ r_f &= \text{risk free rate of return} \ \beta_i &= \text{systematic risk} \end{align}

To estimate

Where \(R_i, R_m\) are observed rates of return

Let

\begin{align} Y_i = R_i - r_f = \text{rate of return on security i in excess of the risk-free rate of return}\ X_i = R_m - r_f = \text{rate of return on market in excess of the risk-free rate of return} \end{align}

df4 <- read_excel("data/Table2_15.xls")

head(df4,3)

dim(df4)

| y | x |

|---|---|

| <dbl> | <dbl> |

| 6.080228 | 7.263448 |

| -0.924186 | 6.339896 |

| -3.286174 | -9.285217 |

- 240

- 2

model11 <- lm(y ~ 0 + x, data = df4)

model12 <- lm(y ~ x, data = df4)

tidy(model11)

glance(model11)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| x | 1.155512 | 0.07439562 | 15.532 | 4.405444e-38 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.5023352 | 0.5002529 | 5.548786 | NA | NA | NA | -751.3032 | 1506.606 | 1513.568 | 7358.578 | 239 | 240 |

Raw \(R^2\): 0.5

proportion of variation around the origin

tidy(model12)

glance(model12)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | -0.4474811 | 0.36294281 | -1.232925 | 2.188203e-01 |

| x | 1.1711284 | 0.07538643 | 15.535004 | 4.752177e-38 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.5034802 | 0.501394 | 5.542759 | 241.3363 | 4.752177e-38 | 1 | -750.5392 | 1507.078 | 1517.52 | 7311.877 | 238 | 240 |

as.numeric(tidy(model12)[[1,'p.value']])

Intercept: not significant, use model11 instead

Measures of goodness of fit#

print(paste("R Squared: ",glance(model12)$r.squared))

[1] "R Squared: 0.503480169868958"

print(paste("Adjusted R Squared: ",glance(model12)$adj.r.squared))

[1] "Adjusted R Squared: 0.501393952095298"

print(paste("Akaike's Information Criteria: ", glance(model12)$AIC))

[1] "Akaike's Information Criteria: 1507.07843469119"

print(paste("Schwarz’s Information Criterion:",glance(model12)$BIC))

[1] "Schwarz’s Information Criterion: 1517.52035146121"

print(paste("Log Likelihood:",glance(model12)$logLik))

[1] "Log Likelihood: -750.539217345594"

colnames(glance(model12))

- 'r.squared'

- 'adj.r.squared'

- 'sigma'

- 'statistic'

- 'p.value'

- 'df'

- 'logLik'

- 'AIC'

- 'BIC'

- 'deviance'

- 'df.residual'

- 'nobs'

Exercises#

2.1#

Consider the following production function, known in the literature as the transcendental production function (TPF)

\(\text{where Q, L, and K represent output, labor, and capital, respectively}\)

a#

How would you linearize this function?

b#

What is the interpretation of the various coefficients in the TPF?

\(\beta_1\): y intercept

labor: elasticity = \(\beta_2 + \beta_4 L_i\)

capital:: elasticity = \(\beta_3 + \beta_5 K_i\)

c#

Given the data in Table 2.1, estimate the parameters of the TPF

df5 <- read_excel("G:/Datasets/Econometrics BY Example/Excel/Table2_1.xls")

head(df5)

| obs | output | labor | capital | lnoutput | lnlabor | lncapital | lnoutlab | lncaplab | outputstar | capitalstar | laborstar |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> |

| 1 | 38372840 | 424471 | 2689076 | 17.46286 | 12.958599 | 14.80471 | 4.504261 | 1.846109 | -0.1079874 | 0.06368887 | 0.1343891 |

| 2 | 1805427 | 19895 | 57997 | 14.40631 | 9.898224 | 10.96815 | 4.508084 | 1.069923 | -0.9230660 | -0.90551400 | -0.9410533 |

| 3 | 23736129 | 206893 | 2308272 | 16.98251 | 12.239957 | 14.65201 | 4.742552 | 2.412053 | -0.4342360 | -0.07658678 | -0.4439759 |

| 4 | 26981983 | 304055 | 1376235 | 17.11068 | 12.624964 | 14.13486 | 4.485716 | 1.509898 | -0.3618868 | -0.41991854 | -0.1857003 |

| 5 | 217546032 | 1809756 | 13554116 | 19.19792 | 14.408703 | 16.42220 | 4.789218 | 2.013498 | 3.8857391 | 4.06601191 | 3.8167481 |

| 6 | 19462751 | 180366 | 1790751 | 16.78401 | 12.102743 | 14.39815 | 4.681270 | 2.295402 | -0.5294886 | -0.26722449 | -0.5144899 |

model13 <- lm(lnoutput ~ lnlabor + lncapital + labor + capital, data = df5)

tidy(model13)

glance(model13)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | 3.949841e+00 | 5.660371e-01 | 6.9780608 | 9.829494e-09 |

| lnlabor | 5.208141e-01 | 1.347469e-01 | 3.8651277 | 3.465680e-04 |

| lncapital | 4.717828e-01 | 1.231899e-01 | 3.8297200 | 3.865161e-04 |

| labor | -2.519414e-07 | 4.201003e-07 | -0.5997173 | 5.516375e-01 |

| capital | 3.552743e-08 | 5.299532e-08 | 0.6703880 | 5.059624e-01 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9645228 | 0.9614378 | 0.271165 | 312.6518 | 1.032818e-32 | 4 | -3.17825 | 18.3565 | 29.94745 | 3.382401 | 46 | 51 |

(intercept <-exp(tidy(model13)[[1,2]]))

df5 |>

summarize(mean_labor = mean(labor),

mean_capital = mean(capital))

| mean_labor | mean_capital |

|---|---|

| <dbl> | <dbl> |

| 373914.5 | 2516181 |

print(paste("elasticity of labor at mean:",5.208141e-01+ -2.519414e-07*373914.5 ))

[1] "elasticity of labor at mean: 0.4266095573897"

d#

Suppose you want to test the hypothesis that B4 = B5 = 0. How would you test these hypotheses? Show the necessary calculations.

full_model <- lm(log(output) ~ log(labor) + log(capital) + labor + capital, data = df5)

restricted_model <- lm(log(output) ~ log(labor) + log(capital), data = df5)

(anova_result <- anova(restricted_model, full_model))

f_statistic <- anova_result$F[2]

p_value <- anova_result$`Pr(>F)`[2]

cat("F-statistic:", f_statistic, "\n")

cat("P-value:", p_value, "\n")

if (p_value < 0.05) {

cat("Reject the null hypothesis: There is evidence that at least one of beta_4 or beta_5 is not equal to zero.\n")

} else {

cat("Fail to reject the null hypothesis: There is no evidence that beta_4 or beta_5 are different from zero.\n")

}

| Res.Df | RSS | Df | Sum of Sq | F | Pr(>F) | |

|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | |

| 1 | 48 | 3.415520 | NA | NA | NA | NA |

| 2 | 46 | 3.382404 | 2 | 0.03311649 | 0.2251887 | 0.7992404 |

F-statistic: 0.2251887

P-value: 0.7992404

Fail to reject the null hypothesis: There is no evidence that beta_4 or beta_5 are different from zero.

e#

How would you compute the output-labor and output capital elasticities for this model? Are they constant or variable?

variable