6. Autocorrelation#

suppressPackageStartupMessages({

library(tidyverse)

library(tidymodels)

library(readxl)

library(multcomp)

library(car)

library(lmtest)

library(sandwich)

})

US Consumption function 1947-2000#

df <- read_excel("data/Table6_1.xls")

head(df)

| year | consumption | income | wealth | interest | lnconsump | lndpi | lnwealth | dlnconsump | dlndpi | ⋯ | rlnwealth | rinterest | dconsump | dincome | dwealth | rconsump | rincome | rwealth | rinterest2 | time |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | ⋯ | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> |

| 21916 | 976.4 | 1035.2 | 5166.815 | -10.350940 | 6.883873 | 6.942350 | 8.550012 | NA | NA | ⋯ | NA | NA | NA | NA | NA | NA | NA | NA | NA | 1 |

| 21916 | 998.1 | 1090.0 | 5280.757 | -4.719804 | 6.905853 | 6.993933 | 8.571825 | 0.02198076 | 0.051583290 | ⋯ | 5.795887 | -1.35915709 | 21.69995 | 54.800049 | 113.9419 | 704.3560 | 778.5664 | 3726.352 | -1.60578680 | 2 |

| 21916 | 1025.3 | 1095.6 | 5607.351 | 1.044063 | 6.932741 | 6.999057 | 8.631834 | 0.02688742 | 0.005124092 | ⋯ | 5.848814 | 2.57644486 | 27.20007 | 5.599976 | 326.5942 | 725.0278 | 767.6801 | 4018.668 | 2.46398711 | 3 |

| 21916 | 1090.9 | 1192.7 | 5759.515 | 0.407346 | 6.994758 | 7.083975 | 8.658608 | 0.06201744 | 0.084917545 | ⋯ | 5.856105 | 0.06836937 | 65.59998 | 97.099976 | 152.1641 | 782.4448 | 863.0954 | 4072.578 | 0.09324604 | 4 |

| 21916 | 1107.1 | 1227.0 | 6086.056 | -5.283152 | 7.009499 | 7.112328 | 8.713756 | 0.01474094 | 0.028352737 | ⋯ | 5.902559 | -5.41540527 | 16.19995 | 34.300049 | 326.5410 | 778.9094 | 868.1835 | 4353.341 | -5.40569973 | 5 |

| 21916 | 1142.4 | 1266.8 | 6243.864 | -0.277011 | 7.040886 | 7.144249 | 8.739354 | 0.03138733 | 0.031921864 | ⋯ | 5.910253 | 1.43827367 | 35.30005 | 39.800049 | 157.8076 | 809.3358 | 897.6646 | 4412.911 | 1.31239307 | 6 |

colnames(df)

- 'year'

- 'consumption'

- 'income'

- 'wealth'

- 'interest'

- 'lnconsump'

- 'lndpi'

- 'lnwealth'

- 'dlnconsump'

- 'dlndpi'

- 'dlnwealth'

- 'dinterest'

- 'rlnconsump'

- 'rlndpi'

- 'rlnwealth'

- 'rinterest'

- 'dconsump'

- 'dincome'

- 'dwealth'

- 'rconsump'

- 'rincome'

- 'rwealth'

- 'rinterest2'

- 'time'

real consumption expenditure (C),

real (after tax) disposable personal income (DPI),

real wealth (W)

and real interest rate (R)

model <- lm(lnconsump ~ lndpi + lnwealth + interest, data =df)

tidy(model)

glance(model)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | -0.467712044 | 0.0427779986 | -10.933472 | 7.330410e-15 |

| lndpi | 0.804872759 | 0.0174978490 | 45.998383 | 1.376236e-42 |

| lnwealth | 0.201270215 | 0.0175925850 | 11.440628 | 1.433544e-15 |

| interest | -0.002689061 | 0.0007619294 | -3.529279 | 9.046458e-04 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9995597 | 0.9995332 | 0.01193375 | 37832.66 | 7.120776e-84 | 3 | 164.588 | -319.1761 | -309.2312 | 0.007120721 | 50 | 54 |

if real personal disposal income goes up by 1%, mean real consumption expenditure goes up by about 0.8%

if real wealth goes up by 1%, mean real consumption expenditure goes up by about 0.2%,

if rate goes up by one percentage point, mean real consumption expenditure goes down by about 0.26%

\(R^2\) indicating spurious correlation

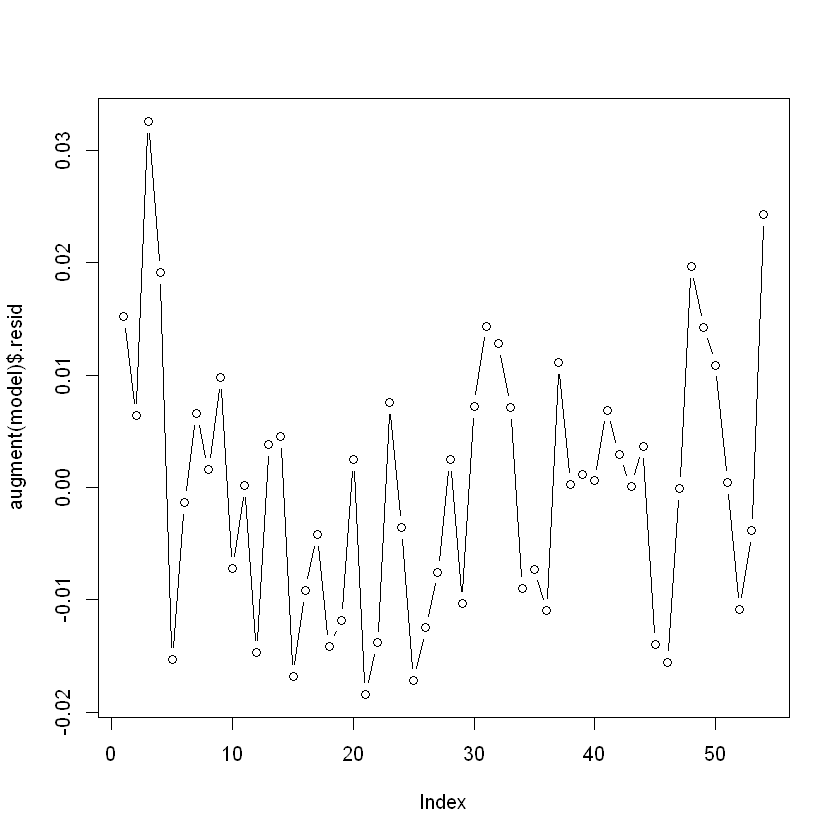

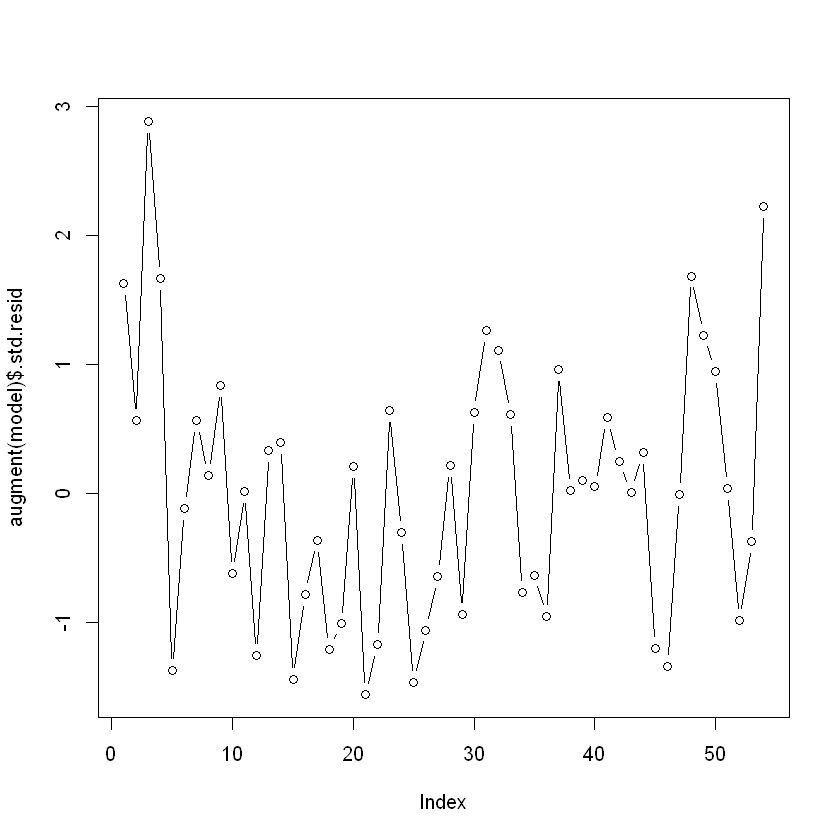

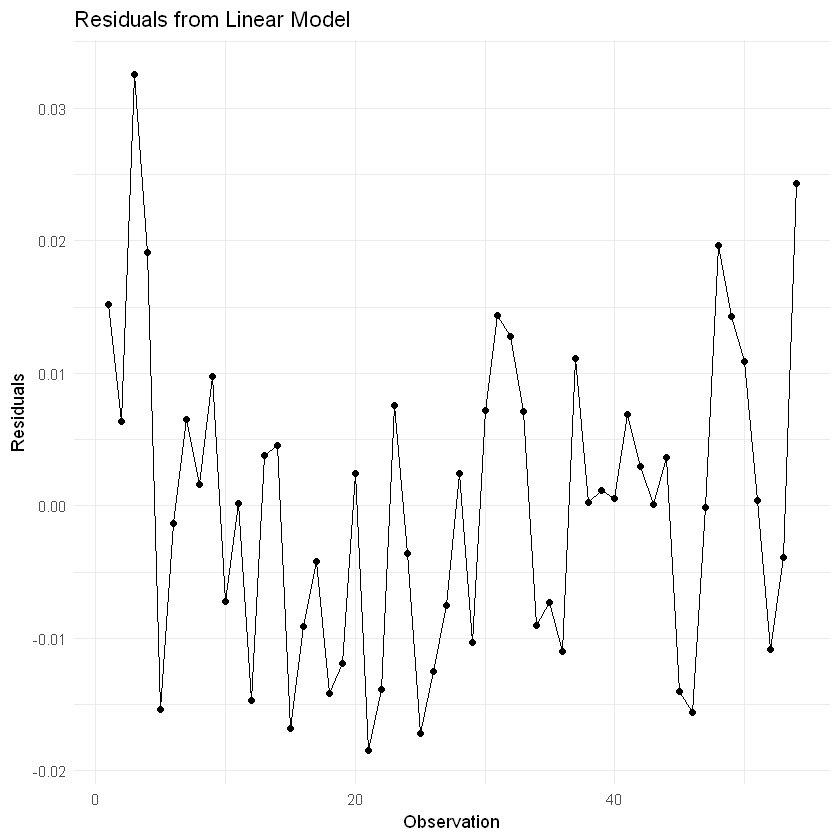

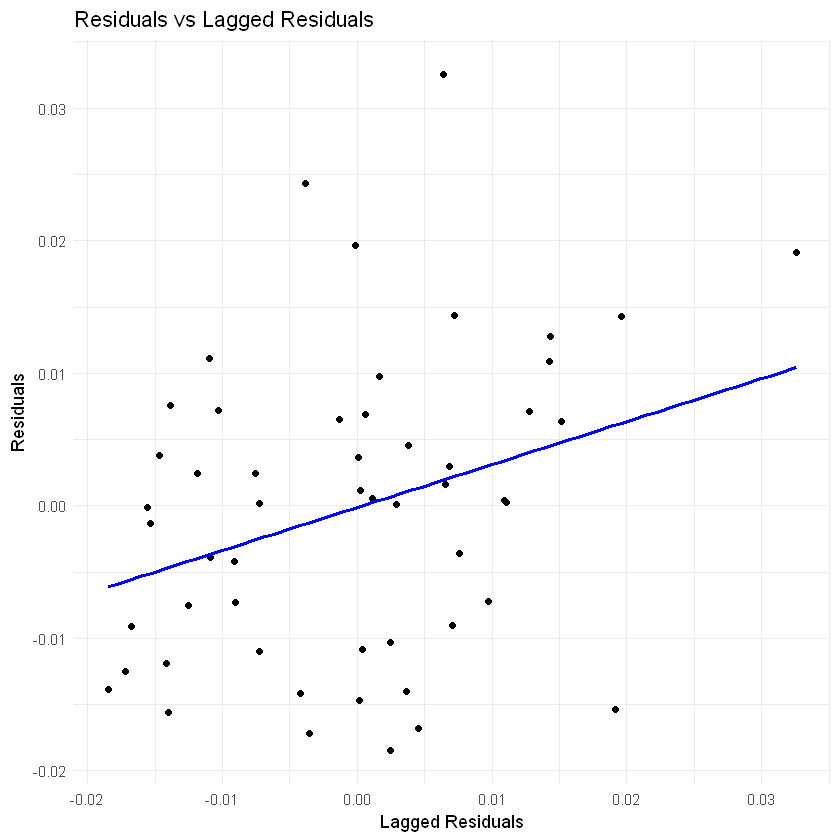

Tests of autocorrelation#

plot(augment(model)$.resid, type = 'b')

plot(augment(model)$.std.resid, type = 'b')

augmented_data <- augment(model)

ggplot(augmented_data, aes(x = seq_along(.resid), y = .resid)) +

geom_line() +

geom_point() +

labs(title = "Residuals from Linear Model",

x = "Observation",

y = "Residuals") +

theme_minimal()

augmented_data <- augmented_data %>%

mutate(lagged_resid = lag(.resid))

# remove first row of NA lagged residual

augmented_data <- augmented_data %>%

filter(!is.na(lagged_resid))

correlation <- cor(augmented_data$.resid, augmented_data$lagged_resid)

ggplot(augmented_data, aes(x = lagged_resid, y = .resid)) +

geom_point() +

geom_smooth(method = "lm",formula = 'y ~ x', se = FALSE, color = "blue") +

labs(title = "Residuals vs Lagged Residuals",

x = "Lagged Residuals",

y = "Residuals") +

theme_minimal()

Durbin watson test#

must have an intercept term

durbinWatsonTest(model)

lag Autocorrelation D-W Statistic p-value

1 0.2977555 1.289232 0

Alternative hypothesis: rho != 0

durbinWatsonTest(model, max.lag = 3)

lag Autocorrelation D-W Statistic p-value

1 0.29775555 1.289232 0.000

2 -0.02840613 1.933710 0.694

3 0.01631809 1.678649 0.262

Alternative hypothesis: rho[lag] != 0

dwtest(model)

Durbin-Watson test

data: model

DW = 1.2892, p-value = 0.0009445

alternative hypothesis: true autocorrelation is greater than 0

Bruech Godfrey general test#

bgtest(model, order = 1)

Breusch-Godfrey test for serial correlation of order up to 1

data: model

LM test = 5.312, df = 1, p-value = 0.02118

bgtest(model, order = 2)

Breusch-Godfrey test for serial correlation of order up to 2

data: model

LM test = 6.4472, df = 2, p-value = 0.03981

bgtest(model, order = 3)

Breusch-Godfrey test for serial correlation of order up to 3

data: model

LM test = 6.6573, df = 3, p-value = 0.08366

AR(2) is significant, residuals follow AR(2)

Remedial measures#

First Difference#

\begin{align} \ln C_t- \rho \ln C_{t-1}&= \beta_{1(1- \rho)} \ &+ \beta_2 (\ln DPI_t - \rho \ln DPI_{t-1})\ &+ \beta_3 (\ln W_t - \rho \ln W_{t-1}) \ &+ \beta_4 (R_t - R_{t-1}) \ &+ (u_t - \rho u_{t-1}) \end{align}

if \(\rho\) = 1

Called first difference transformation

model2 <- lm(diff(lnconsump) ~ 0 +diff(lndpi) + diff(lnwealth) + diff(interest), data =df)

tidy(model2)

glance(model2)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| diff(lndpi) | 0.8489940413 | 0.0515376309 | 16.4732842 | 7.667028e-22 |

| diff(lnwealth) | 0.1063549555 | 0.0368543147 | 2.8858210 | 5.749199e-03 |

| diff(interest) | 0.0006530138 | 0.0008260853 | 0.7904919 | 4.329740e-01 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9236527 | 0.9190718 | 0.0111335 | 201.6339 | 6.473553e-28 | 3 | 164.7236 | -321.4472 | -313.5661 | 0.006197738 | 50 | 53 |

bgtest(model2)

Breusch-Godfrey test for serial correlation of order up to 1

data: model2

LM test = 0.86275, df = 1, p-value = 0.353

dwtest(model2)

Durbin-Watson test

data: model2

DW = 2.0265, p-value = 0.547

alternative hypothesis: true autocorrelation is greater than 0

durbinWatsonTest(model2)

lag Autocorrelation D-W Statistic p-value

1 -0.1150018 2.026542 0.916

Alternative hypothesis: rho != 0

feasible generalized least squares (FGLS)#

residuals = augment(model)$.resid

residuals

- 0.0151792320906274

- 0.00639409190557938

- 0.0325786316647871

- 0.0191471920745867

- -0.0153337901242683

- -0.00132990098127195

- 0.00653719274943132

- 0.00162048925147751

- 0.00975015218633235

- -0.00722925871798008

- 0.000174758857319546

- -0.0146975939327243

- 0.00380689173579718

- 0.00454249958702402

- -0.0167822153758674

- -0.0091399779495811

- -0.00422252846219351

- -0.014143908709439

- -0.011875949295832

- 0.00245712248775831

- -0.0184412867267767

- -0.0138427704324453

- 0.00757496364792853

- -0.00357671809715665

- -0.0171562076207774

- -0.0124861952550575

- -0.00754242394929072

- 0.00245643437586018

- -0.0102882063980623

- 0.00718617423785339

- 0.0143585227051846

- 0.0127678086817866

- 0.0070919535900682

- -0.00903155158175295

- -0.00726634215564381

- -0.0109670199434095

- 0.0110890173466256

- 0.000254097439515988

- 0.00116108304687401

- 0.000586076244815104

- 0.00687811518401915

- 0.00293814373603141

- 8.79859166129648e-05

- 0.00366504301640092

- -0.0140024869709681

- -0.0155797023743123

- -0.00012753645438579

- 0.0196279528980181

- 0.0142734120216019

- 0.0108911843032331

- 0.000420259520168997

- -0.0108587536823013

- -0.00387038232170589

- 0.024296225009854

rho <- coef(lm(residuals ~ 0 + lag(residuals)))

rho

dwtest(model)

Durbin-Watson test

data: model

DW = 1.2892, p-value = 0.0009445

alternative hypothesis: true autocorrelation is greater than 0

durbinWatsonTest(model)

lag Autocorrelation D-W Statistic p-value

1 0.2977555 1.289232 0.004

Alternative hypothesis: rho != 0

rho2 = 1 - (1.289232/2)

rho2

fgls_model <- lm(I(lnconsump-rho*lag(lnconsump)) ~ I(lndpi-rho*lag(lndpi)) +

I(lnwealth-rho*lag(lnwealth)) + I(interest-rho*lag(interest)) , data = df)

tidy(fgls_model)

glance(fgls_model)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | -2.797310e-01 | 0.033726467 | -8.2941093 | 6.807447e-11 |

| I(lndpi - rho * lag(lndpi)) | 8.187056e-01 | 0.021096888 | 38.8069362 | 1.878713e-38 |

| I(lnwealth - rho * lag(lnwealth)) | 1.836285e-01 | 0.020987236 | 8.7495302 | 1.396990e-11 |

| I(interest - rho * lag(interest)) | -1.799604e-05 | 0.000969139 | -0.0185691 | 9.852603e-01 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9992348 | 0.999188 | 0.0104226 | 21330.12 | 2.542681e-76 | 3 | 168.756 | -327.512 | -317.6606 | 0.005322902 | 49 | 53 |

bgtest(fgls_model)

Breusch-Godfrey test for serial correlation of order up to 1

data: fgls_model

LM test = 2.8168, df = 1, p-value = 0.09328

dwtest(fgls_model)

Durbin-Watson test

data: fgls_model

DW = 1.449, p-value = 0.008542

alternative hypothesis: true autocorrelation is greater than 0

durbinWatsonTest(fgls_model)

lag Autocorrelation D-W Statistic p-value

1 0.2092955 1.448986 0.014

Alternative hypothesis: rho != 0

library(dynlm)

# Create the FGLS formula

fgls_formula <- as.formula(paste("I(lnconsump - ", rho, "* lag(lnconsump)) ~ ",

"I(lndpi - ", rho, "* lag(lndpi)) + ",

"I(lnwealth - ", rho, "* lag(lnwealth)) + ",

"I(interest - ", rho, "* lag(interest))"

))

# Fit the FGLS model using dynlm

fgls_model <- dynlm(fgls_formula, data = df)

# Tidy model coefficients

tidy(fgls_model)

# Model summary

glance(fgls_model)

Warning message:

"The `tidy()` method for objects of class `dynlm` is not maintained by the broom team, and is only supported through the `lm` tidier method. Please be cautious in interpreting and reporting broom output.

This warning is displayed once per session."

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | -2.797310e-01 | 0.033726467 | -8.2941093 | 6.807447e-11 |

| I(lndpi - 0.324670692527429 * lag(lndpi)) | 8.187056e-01 | 0.021096888 | 38.8069362 | 1.878713e-38 |

| I(lnwealth - 0.324670692527429 * lag(lnwealth)) | 1.836285e-01 | 0.020987236 | 8.7495302 | 1.396990e-11 |

| I(interest - 0.324670692527429 * lag(interest)) | -1.799604e-05 | 0.000969139 | -0.0185691 | 9.852603e-01 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9992348 | 0.999188 | 0.0104226 | 21330.12 | 2.542681e-76 | 3 | 168.756 | -327.512 | -317.6606 | 0.005322902 | 49 | 53 |

library(dynlm)

# Fit the original model

model <- lm(lnconsump ~ lndpi + lnwealth + interest, data = df)

# Get residuals

residuals <- residuals(model)

# Estimate AR(2) coefficients

ar_model <- lm(residuals ~ lag(residuals, 1) + lag(residuals, 2))

rho1 <- coef(ar_model)[2]

rho2 <- coef(ar_model)[3]

# Create the FGLS formula for AR(2)

fgls_formula <- as.formula(paste("I(lnconsump - ", rho1, "* lag(lnconsump, 1) - ", rho2, "* lag(lnconsump, 2)) ~ ",

"I(lndpi - ", rho1, "* lag(lndpi, 1) - ", rho2, "* lag(lndpi, 2)) + ",

"I(lnwealth - ", rho1, "* lag(lnwealth, 1) - ", rho2, "* lag(lnwealth, 2)) + ",

"I(interest - ", rho1, "* lag(interest, 1) - ", rho2, "* lag(interest, 2))"

))

fgls_model <- lm(fgls_formula, data = df)

tidy(fgls_model)

glance(fgls_model)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | -0.3402025749 | 0.037997412 | -8.9533091 | 8.307709e-12 |

| I(lndpi - 0.375966677578179 * lag(lndpi, 1) - -0.159419476639279 * lag(lndpi, 2)) | 0.8121613433 | 0.019923567 | 40.7638520 | 6.679649e-39 |

| I(lnwealth - 0.375966677578179 * lag(lnwealth, 1) - -0.159419476639279 * lag(lnwealth, 2)) | 0.1913213476 | 0.019988221 | 9.5717046 | 1.040704e-12 |

| I(interest - 0.375966677578179 * lag(interest, 1) - -0.159419476639279 * lag(interest, 2)) | -0.0007507104 | 0.001005589 | -0.7465382 | 4.589834e-01 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9993667 | 0.9993271 | 0.01078611 | 25247.09 | 9.734735e-77 | 3 | 163.8301 | -317.6602 | -307.904 | 0.005584327 | 48 | 52 |

Newey–West method of correcting OLS standard errors#

NeweyWest(model)

| (Intercept) | lndpi | lnwealth | interest | |

|---|---|---|---|---|

| (Intercept) | 1.971479e-03 | 2.692235e-05 | -2.333159e-04 | 2.652791e-05 |

| lndpi | 2.692235e-05 | 2.628983e-04 | -2.225614e-04 | -6.845951e-06 |

| lnwealth | -2.333159e-04 | -2.225614e-04 | 2.109662e-04 | 2.866692e-06 |

| interest | 2.652791e-05 | -6.845951e-06 | 2.866692e-06 | 6.724860e-07 |

Model Evaluation#

consider case of specification error

model4 <- lm(lnconsump ~ log(income) + lnwealth + interest + lag(lnconsump), data =df)

tidy(model4)

glance(model4)

| term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> |

| (Intercept) | -0.316021364 | 0.0556667072 | -5.6770264 | 7.777927e-07 |

| log(income) | 0.574833115 | 0.0696731710 | 8.2504227 | 9.237758e-11 |

| lnwealth | 0.150288163 | 0.0208376010 | 7.2123544 | 3.477275e-09 |

| interest | -0.000675206 | 0.0008937643 | -0.7554632 | 4.536624e-01 |

| lag(lnconsump) | 0.276561599 | 0.0804719157 | 3.4367468 | 1.225013e-03 |

| r.squared | adj.r.squared | sigma | statistic | p.value | df | logLik | AIC | BIC | deviance | df.residual | nobs |

|---|---|---|---|---|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <int> | <int> |

| 0.9996454 | 0.9996159 | 0.01061906 | 33833.64 | 3.891148e-82 | 4 | 168.3127 | -324.6254 | -312.8037 | 0.005412694 | 48 | 53 |

bgtest(model4)

Breusch-Godfrey test for serial correlation of order up to 1

data: model4

LM test = 4.4804, df = 1, p-value = 0.03429

Exercises#

🚧 Under Construction